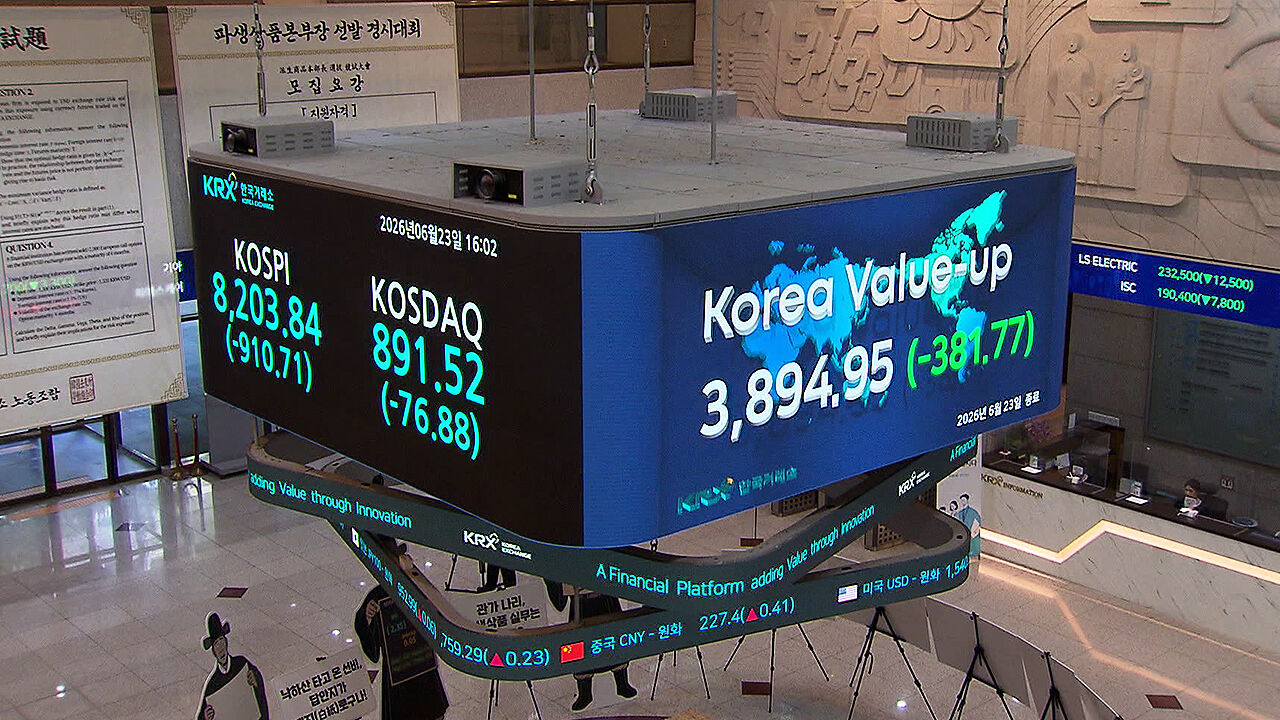

What Are the Negative Factors That Caused a Historic Stock Market Crash?

① Side Effects of Semiconductor Concentration and Profit-Taking Sell-Off

The Kospi's recent climb past 9,100 was essentially a two-horse race led by the dual powerhouses of Samsung Electronics and SK Hynix. This has now backfired. News of large-scale fundraising by AI-related Big Tech companies in New York fueled anxiety. As doubts spread over whether these investments would yield sufficient returns, tech stocks on Wall Street plummeted, dealing a heavy blow to the twin engines of the Korean stock market. Foreign investors dumped massive volumes of large-cap semiconductor shares.

② Delay in SK Hynix ADR Listing Review

News that the U.S. Securities and Exchange Commission (SEC) has once again delayed its review of SK Hynix's American Depositary Receipts (ADR) listing was another blow. As the event, which had been highly anticipated as a gateway for global capital inflows, became uncertain, disappointed global passive funds and hedge funds quickly pulled their money out.

③ Weakening Won (Surging Exchange Rate) and Fear of Foreign Exchange Losses

As tensions in the Strait of Hormuz escalated due to conflicts between the U.S. and Iran, demand for the U.S. dollar, a representative safe-haven asset, skyrocketed. With the trend of capital returning to the dollar already growing, the surging won-dollar exchange rate left foreign investors facing the double whammy of falling stock prices and potential foreign exchange losses.

④ Runaway Mechanical Sell-Offs via Program Trading

The failure to be included in the MSCI index, combined with the instability in Hormuz, maximized downward pressure through futures-and-options-linked program trading centered on large-cap stocks—a chronic weakness of the domestic market. Ultimately, when the index broke below key support levels, a flood of mechanical stop-loss orders was triggered.

Single-Stock 2x Leverage ETFs: Growing into Stock Market Monsters

① A 'Black Hole' Sucking in Capital

At the time of their listing in late May, the total net assets of the 16 listed products were relatively small, hovering around 200 billion to 300 billion won each. However, over the past month, they have acted like a 'black hole' for market liquidity. As of June 22, the total market capitalization of all 16 products reached 12.3 trillion won, roughly tripling since their debut. The pace of capital inflow has completely overwhelmed the early listing records of conventional index-based ETFs.

② Extreme Concentration of Trading Volume

Since the listing of single-stock leverage ETFs, cumulative trading volume has reached approximately 142.7 trillion won, with an average of 8.4 trillion won changing hands daily in this market. This accounts for a staggering 23% of the total ETF trading volume of approximately 622 trillion won during the same period. A severe market distortion has emerged, with just 16 single-stock leverage products monopolizing nearly a quarter of all ETF trading in the domestic stock market.

③ 'Tornado-Like' Daily Turnover Ratio

The Financial Supervisory Service (FSS) recently revealed that the daily turnover ratio of single-stock leverage ETFs averaged 122.5% up to June 12. This is more than four times higher than the 30.2% average turnover of domestic stock-based leverage and inverse ETFs, let alone the spot stock turnover of Samsung Electronics and SK Hynix, which stands at less than 1%. In extreme cases, the turnover ratio neared 200%. This means that short-term trading was so intense that the entire outstanding shares of these ETFs changed hands twice in a single day.

Single-Stock Leverage ETFs Unleash Their Destructive Power

① Triggering a Deluge of Hedging Sell Orders from Liquidity Providers (LPs)

To guarantee a 2x return to investors, asset management companies and LPs operating leverage ETFs must hold the underlying stocks or related derivatives (such as futures). However, when stock prices plummet, LPs are forced to sell the underlying Samsung Electronics or SK Hynix shares and futures in the market to maintain the leverage debt ratio owed to investors. As the index crumbled and the stock prices of both companies plunged during yesterday's trading, single-stock leverage ETFs dumped massive program hedging sell orders to defend their asset value. This exacerbated the decline of the two large-cap stocks, creating a vicious cycle that dragged the Kospi index even deeper into the abyss.

② Late-Session Sell-Offs Driven by Daily Rebalancing

Leverage ETFs adjust their portfolios at the close of every trading day to match 'twice the daily return,' a process known as rebalancing. On days when stock prices crash throughout the session, like yesterday, these funds are structurally required to sell off massive amounts of underlying futures right before the market closes to maintain their leverage ratio. Indeed, it has been confirmed that a significant portion of the abnormal selling pressure on Samsung Electronics and SK Hynix near the closing call yesterday was driven by the mechanical rebalancing sales of these leverage ETFs.

③ Driving an Explosive Rise in the Fear Index

Because the market capitalization of these two underlying stocks is so dominant in the Kospi, the volatility triggered by their leverage products quickly infected the entire market. Yesterday, the Kospi 200 Volatility Index—often dubbed Korea's fear index—approached the 90 level to hit a yearly high. This serves as decisive proof that the explosion of large-cap volatility triggered by single-stock leverage ETFs paralyzed overall investor sentiment.

Analysts point to the recently introduced 'single-stock 2x leverage ETF'—a monster derivative product—as the key culprit that maximized the 'wag-the-dog' phenomenon, where the tail wags the dog, during yesterday's crash.

The Financial Supervisory Service's Belated Remedy

Governor Lee's remarks, such as "I should have blocked it even if it meant lying down in protest" and "It only lined the pockets of brokerage firms with commission fees," paradoxically amount to an admission of policy misalignment within the government and a failure of preemptive risk control. This exposed the discord between the FSC, which pushed through the product launch, and the FSS, which failed to warn of the impending volatility explosion on the ground and only issued "belated warnings." As a result of the authorities opening the door to high-risk products without safety nets, the wild swings in the domestic stock market are spiraling out of control.

Today, the FSS hurriedly held a meeting with risk management executives from 10 major domestic brokerage firms, in cooperation with the Korea Financial Investment Association. The FSS urged brokerage firms not to limit themselves to superficial limit management, but to operate risk management systems that reflect market conditions and the need for investor protection. It emphasized that brokerages should refrain from business practices that lead to margin transactions without investors being fully informed, or practices that virtually induce margin trading. The regulator also ordered brokerages to clearly explain the conditions for forced liquidation (margin calls) and the potential scope of losses so that investors can easily understand them, and to strengthen their compliance with the duty to explain terms and conditions and product prospectuses. This is a classic case of neglecting the root to chase the branches, and prescribing medicine after the patient has died. Going forward, the financial authorities will likely be left to agonize over how to control the tail that is wagging the dog.

※ Please note: This article was translated by AI and may contain errors.

Video News

Video News

Video News

Video News

Video News

Video News