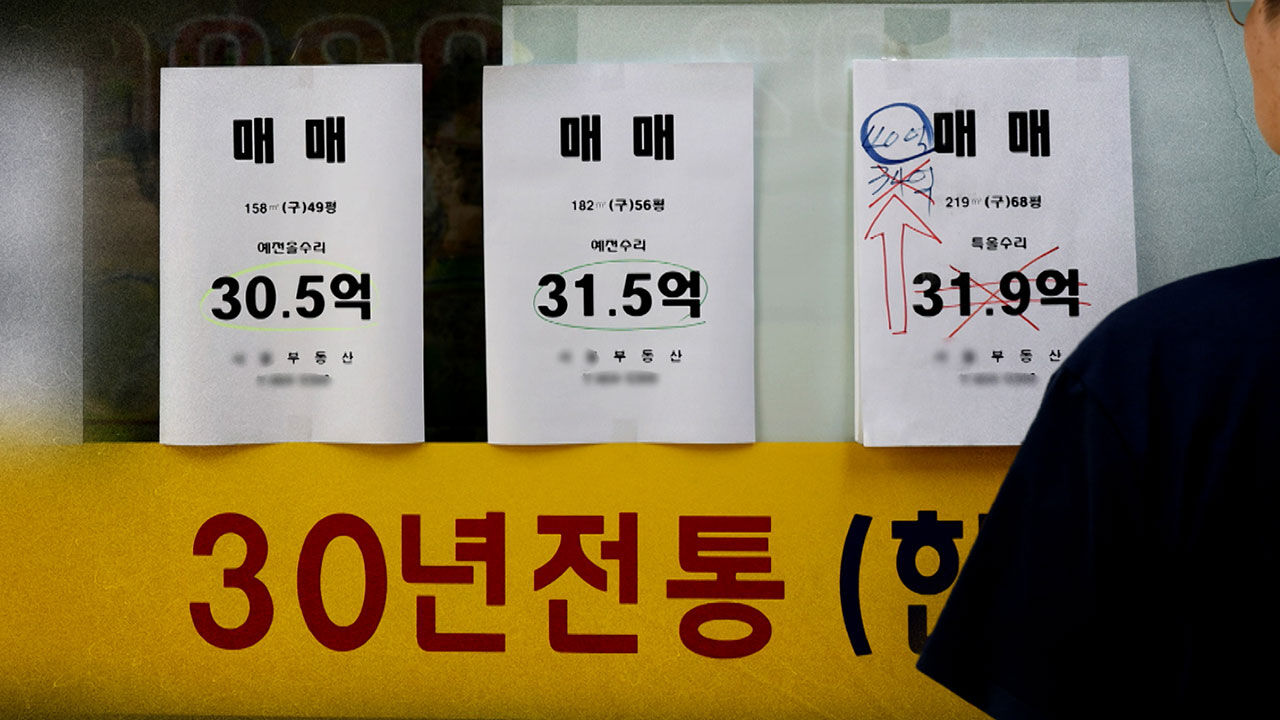

The Bank of Korea (BOK) has issued a warning that rising housing prices, particularly in the Seoul metropolitan area, and an increase in "debt-financed investing" (borrowing to invest in stocks) amid a strong stock market could threaten financial stability.

In its Financial Stability Report released today (June 24), the Bank of Korea stated, "Amid significantly increased volatility in domestic financial and foreign exchange markets, key risk factors include the renewed upward trend in housing prices in the capital region, the potential for accumulating financial imbalances due to increased leveraged asset investments, and concerns over rising defaults in vulnerable sectors following changes in financial conditions such as interest rate hikes."

The Financial Stress Index (FSI), which reflects the short-term stability of the financial system, reached 17.2 in May of this year, up from 16.3 in December of last year, remaining in the "caution" stage (12 or higher).

The Financial Vulnerability Index (FVI), which indicates the medium- to long-term fragility of the financial system, also stood at 46.0 in the first quarter of this year, slightly exceeding the long-term average (45.7 since 2008).

Household credit has increased significantly since May, driven by a rise in housing transactions—which were reflected in loan figures with a time lag ahead of the resumption of heavy capital gains taxes for multi-home owners—as well as an increase in other types of loans, including credit loans.

The average monthly increase in household loans has expanded notably, rising from 2.7 trillion won between October and December last year to 3 trillion won from January to March this year, 3.5 trillion won in April, and 9.3 trillion won in May.

However, the household debt-to-disposable income ratio (DTI) at the end of the first quarter of this year is estimated to have fallen significantly to 134.1%, compared to 139.7% at the end of the third quarter of last year.

The household delinquency rate also stood at 1.00% at the end of the first quarter, remaining below the long-term average of 1.16%.

The delinquency rate for corporate loans turned upward to 2.43% at the end of January this year, significantly exceeding the long-term average of 1.62%.

Polarization between companies has become more pronounced.

The interest coverage ratio improved for large corporations from 4.0 in 2024 to 5.4 last year, and for small and medium-sized enterprises (SMEs) from -0.7 in 2024 to -0.4; however, SMEs remain in a negative state.

This means their operating profits are still insufficient to cover their total interest expenses.

The Bank of Korea emphasized, "The growth of household credit is expanding again, and regarding the debt repayment capacity of households and corporations, it is necessary to remain mindful that credit risks for vulnerable household borrowers and companies in certain sectors remain high."

※ Please note: This article was translated by AI and may contain errors.

Bank of Korea Warns of Financial Instability Risks Due to Rising Housing Prices and Debt-Financed Investing

Copyright Ⓒ SBS & SBSi. All rights reserved.

Copying, redistribution, and unauthorized use in AI training are strictly prohibited.

Copying, redistribution, and unauthorized use in AI training are strictly prohibited.

Trending Now

-

Video News

Video News

Middle Schoolers Stabbed, Yet Police "Walked Like They Were Heading to Lunch": Controversy Over Response Footage

-

Video News

7.3 Billion Won in Taxpayer Money Already Paid... Daejeon on High Alert Over "Near-Bankruptcy" Crisis

-

Video News

First Grader Commits Sexual Assault? Public Outrage Boils Over Calls to Abolish Juvenile Exemption

-

Escaped Wolf-Dog Spotted in Dangjin After Fleeing Seosan? "Do Not Approach, Report Immediately"

-

Photos of 19-Month-Old Girl Who Died of Neglect Released: Emaciated Body and Sunken Eyes

Video News

Video News

Video News

Video News

Video News

Video News