SBS뉴스

Where Is the Peak of the Semiconductor Rally? Stock Market Enters Lean Times

입력 : 2026.07.07 18:22

Foreigners Sell Off Heavily Despite Samsung Electronics' 89 Trillion Won Q2 Operating Profit

Market participants are facing growing dilemmas. Although the unprecedentedly strong earnings of South Korea's top two semiconductor giants are said to have been priced in, worrying about a "peak-out" in the semiconductor industry seems premature given that demand is already solid through next year due to long-term contracts. Yet, those concerns are surfacing too quickly. Ultimately, after a period of profit-taking from short-term surges and stock price corrections, this summer is expected to be a testing ground to gauge whether the market will enter a second rally in the second half of the year, starting with the earnings reports of big tech companies from mid-this month to next month.

Three Years' Worth of Profit Earned at Once, But an Unexpected 'Sell-on'

In fact, while the first-quarter earnings were also an "earning surprise," the stock price fell on the day of the announcement. Analysts first point to the market's "sell-on" phenomenon, where selling occurs even when good news breaks. Since the stock price had already risen on expectations of strong earnings, profit-taking sentiment driven by the perception of "exhausted momentum" was strong, particularly among foreign investors. Indeed, some in the securities industry commented, "Although the announced figures were slightly better than forecasts, the psychological surprise effect was halved amid vague, high expectations for a 100 trillion won performance." Some also explain that concerns over the relative sluggishness of the non-memory semiconductor and mobile (DX) divisions were reflected, given Samsung Electronics' revenue structure as an integrated IT company. Nevertheless, the view that signs of change in the market environment surrounding the semiconductor industry are having a full-fledged impact is gaining traction, as evidenced by the relentless selling by foreign investors.

Is the Peak Nearing? Signs of Pushback Against DRAM Dominance

Another piece of news was the case of Meta. As the hyperscaler, which has been going all-in on AI infrastructure investment, was reported to be preparing a strategy to sell some of its data center "computing" resources to external parties, concerns arose that AI infrastructure investment—previously perceived as being in absolute shortage—might actually be overcapacity. Although this policy was not officially announced by Meta, Bloomberg's report caused a larger-than-expected ripple effect. If Meta's AI computing capacity is indeed in surplus as feared, Meta would not need to purchase more AI accelerator chips like Nvidia's GPUs, which would also impact the demand for the semiconductors used in them. However, reality seems to differ significantly from these concerns.

Leasing data centers is a business that Amazon, Google, and Microsoft are already engaged in. Because shareholders and the market constantly raise questions about the realization of profitability from massive infrastructure investments, this is a way to mitigate risks by generating revenue through cloud services using completed facilities. Unlike other hyperscalers, Meta has been building computing infrastructure (data centers) without offering its own cloud services, so this can be seen as a strategy to enter the cloud service market and dispel concerns about profitability. Ultimately, the Meta issue, which acted as a major negative factor for the market, appears to be more of a temporary episode. Looking back, Apple's move to purchase Chinese semiconductors is also a threat to replace expensive South Korean semiconductor supplies, but on the other hand, it signifies how difficult it is to secure essential semiconductor supplies, raising questions about whether it is truly a negative factor.

In a broader context, these issues, which deviate from the mainstream trend, reflect the dilemmas of AI big tech companies suffering from the burden of massive infrastructure investment costs. In the U.S. industry, media, and administration, where the domestic memory semiconductor production base is weak, there is a growing desire to check the rapidly rising prices and supply structures of Taiwanese and South Korean DRAM, and signs of this are beginning to appear.

In a broader context, these issues, which deviate from the mainstream trend, reflect the dilemmas of AI big tech companies suffering from the burden of massive infrastructure investment costs. In the U.S. industry, media, and administration, where the domestic memory semiconductor production base is weak, there is a growing desire to check the rapidly rising prices and supply structures of Taiwanese and South Korean DRAM, and signs of this are beginning to appear.

SK Hynix's U.S. Listing on July 10 Is Another Hurdle

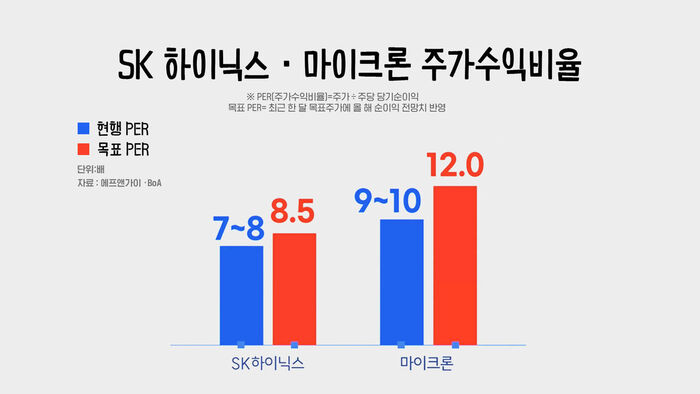

This can be viewed from two perspectives. ① This ADR listing carries concerns of "equity dilution" due to the issuance of new shares from the perspective of existing shareholders. The scale of the ADR issuance is around 42 trillion won, which involves about 17 million new shares, increasing the existing number of shares by about 2%. Therefore, generating sufficient investment demand is essential. The success of the listing can only be judged after observing the newly formed valuation and supply-demand effects in the U.S. market. ② Another key point is that it will be compared in the same market as U.S. semiconductor stocks. Once SK Hynix is traded on the Nasdaq, it will be evaluated alongside memory and storage companies listed on the U.S. stock market, such as Micron, SanDisk, and Seagate. Experts generally project that "considering its overwhelming valuation attractiveness, scale of profits, and technological superiority, this will be a golden opportunity to be reevaluated."

This is because SK Hynix is valued lower than U.S. semiconductor stocks relative to its earnings. According to comparative data based on Bloomberg forecasts, the 12-month forward PER (Price-to-Earnings Ratio) of major global semiconductor companies was recorded at 23.1 times for TSMC, 11.2 times for Micron, and 10.6 times for Japan's Kioxia. In contrast, SK Hynix and Samsung Electronics stood at only 7 times and 6.0 times, respectively. Compared to the average of the three foreign companies, SK Hynix is discounted by about 56%, and Samsung Electronics by about 60%. What matters to retail investors is whether SK Hynix will trade at a higher price in the U.S. stock market compared to its domestic shares. If it trades higher than the converted price of domestic common shares, it indicates that U.S. investor demand is stronger than domestic demand, which could lead to an upward effect on domestic stock prices. However, if the stock price has already priced in the effects of the New York listing, a "sell-on" similar to Samsung Electronics' earnings announcement could occur. If such a trend emerges, there are concerns that semiconductor stock prices could face high volatility again next week.

This is because SK Hynix is valued lower than U.S. semiconductor stocks relative to its earnings. According to comparative data based on Bloomberg forecasts, the 12-month forward PER (Price-to-Earnings Ratio) of major global semiconductor companies was recorded at 23.1 times for TSMC, 11.2 times for Micron, and 10.6 times for Japan's Kioxia. In contrast, SK Hynix and Samsung Electronics stood at only 7 times and 6.0 times, respectively. Compared to the average of the three foreign companies, SK Hynix is discounted by about 56%, and Samsung Electronics by about 60%. What matters to retail investors is whether SK Hynix will trade at a higher price in the U.S. stock market compared to its domestic shares. If it trades higher than the converted price of domestic common shares, it indicates that U.S. investor demand is stronger than domestic demand, which could lead to an upward effect on domestic stock prices. However, if the stock price has already priced in the effects of the New York listing, a "sell-on" similar to Samsung Electronics' earnings announcement could occur. If such a trend emerges, there are concerns that semiconductor stock prices could face high volatility again next week.

The Second Half Is Just Beginning... What Are the Key Variables?

In addition, other burdens include profit-taking sentiment among domestic and foreign semiconductor stock holders, margin calls (forced liquidation) that occur during sharp stock price drops in the domestic market, and the pressure of stock selling due to the National Pension Service's rebalancing, which could sporadically occur in response to negative news related to AI investment. Another burden is the exchange rate. The continuous weakening of the Korean won is a factor driving foreign selling and is putting pressure on domestic interest rate hikes. If the Bank of Korea raises the benchmark interest rate as signaled, it is expected to narrow the interest rate gap with the U.S., but if the Fed raises rates in a hurry, that effect will disappear.

Still Robust 'Chip War'... Too Early for a Peak

In the grand scheme of things, the most crucial variable will be the sustainability of AI investment intensity by U.S. big tech companies. Google's parent company, Alphabet, decided on a capital increase (stock issuance) of over $80 billion last month, departing from its previous pattern of utilizing surplus cash. This suggests that the fierce competition among big tech companies for dominance in the AI industry is advancing to the next level. From South Korea's perspective, while it can expect semiconductor demand to strengthen further for the time being, the point where winners and losers of AI dominance diverge could become an inflection point for DRAM demand, making it necessary to prepare for the approaching finale.

Starting with TSMC's earnings announcement on July 16, followed by Microsoft, Amazon, Google, and SanDisk and Nvidia's earnings announcements in August, these events are expected to serve as indicators to predict the peak of the semiconductor cycle. If big tech companies continue to expand their capital expenditure this quarter, the supercycle will stably continue, but if changes occur, the story will be different.

Industrially, the peak of the so-called semiconductor rally is highly likely to occur as early as the second half of next year, 2027. Although supply is expected to remain short through 2028, the demand structure is highly likely to be reorganized alongside the consolidation of related infrastructure, centered on companies that win the AI dominance race. On the other hand, the peak of the stock market is bound to precede this. While the peak of stock prices can be numerically predicted for the first half of next year, not a few experts advise preparing for the actual peak in October of the second half of this year. Anticipating stock price trends through the industry's peak remains a homework assignment for investors.

※ Please note: This article was translated by AI and may contain errors.

Copyright Ⓒ SBS. All rights reserved. 무단 전재, 재배포 및 AI학습 이용 금지